Acca Insurance Guide: Best Bookmaker Offers Compared 2026

Acca insurance transformed accumulator betting when it first appeared, offering bettors a psychological safety net that softens the brutal disappointment of near-miss losses. The promotion works simply enough if your accumulator loses by exactly one leg while all others win, the bookmaker refunds your stake, usually as a free bet. This single innovation changed how millions of bettors approach accumulators, making the “nine out of ten correct” scenario slightly less devastating.

But acca insurance isn’t charity. Bookmakers introduced these promotions because they’re profitable marketing tools that increase betting volume while maintaining positive expected value for the house. The refund comes with conditions, restrictions, and terms that carefully limit the bookmaker’s liability while encouraging you to place more accumulators than you otherwise would. Understanding how these offers actually work not just how they’re marketed separates bettors who extract genuine value from those who fall into carefully designed behavioral traps.

This comprehensive guide breaks down everything you need to know about acca insurance in 2025. You’ll learn the fundamental mechanics of how refunds work, the different types of insurance promotions bookmakers offer, detailed comparisons of the major UK bookmaker policies, how to calculate whether insurance actually adds value to your betting, strategies for maximizing insurance benefits, and the hidden terms and conditions that can invalidate your refund when you need it most.

Table of Contents

What Is Acca Insurance: The Complete Explanation

Acca insurance sometimes called accumulator insurance, acca protection, or money-back offers is a bookmaker promotion that refunds your stake if your accumulator meets specific failure criteria. The most common structure refunds bets that lose by exactly one selection, meaning all other legs won but a single leg let you down. Some bookmakers extend this to losing by two selections, though those offers are rarer and typically come with additional restrictions.

The refund almost always comes as a free bet rather than cash, which immediately reduces its value compared to your original stake. A twenty-pound cash stake that gets refunded as a twenty-pound free bet isn’t actually equivalent, because the free bet stake isn’t returned when you win. If you use a twenty-pound free bet on odds of 2.00, you get back twenty pounds (the profit) rather than forty pounds (profit plus stake). This means a free bet is worth approximately 80-85% of its face value depending on what odds you can find to use it on.

The mechanics work through automatic detection systems that monitor your accumulator as results settle. If your bet meets the insurance criteria typically a minimum number of selections, minimum odds per leg, and exactly one losing leg the system flags your bet for refund processing. The free bet usually appears in your account within 24-48 hours, though some bookmakers process refunds within minutes of the final result settling.

Different bookmakers structure their insurance requirements differently, but several elements appear almost universally. Minimum selection count typically ranges from four to six legs you can’t get insurance on a simple three-fold. Minimum odds per selection usually sit around 1.20 to 1.40, preventing you from loading your acca with extreme favorites. Maximum refund amounts cap how much you can get back, typically between ten and fifty pounds depending on the bookmaker and your customer status. Qualifying markets vary, with most bookmakers restricting insurance to specific sports or bet types.

The qualifying period matters more than many bettors realize. Some insurance offers apply only to pre-match accumulators placed before the first kick-off. Others allow in-play accumulator construction but require all legs to be placed before any results settle. A few bookmakers let you add selections after earlier legs have won, though these offers typically come with stricter terms. Reading the fine print about when and how you can build your accumulator determines whether your bet qualifies.

Settlement rules affect whether your bet meets insurance criteria in edge cases. If one of your selections is voided due to match postponement, most bookmakers remove that leg and recalculate your acca with the remaining selections. This might mean your five-fold becomes a four-fold, which could fall below the minimum selection count for insurance qualification. Similarly, if multiple selections void, your acca might settle as a winner but the insurance terms required all original legs to have valid results, disqualifying you from any bonus offers attached to the promotion.

Geographic restrictions limit which bettors can access certain insurance offers. UK-facing bookmakers typically offer the best insurance terms because the competitive UK betting market forces aggressive promotions. European bookmakers often have less generous terms, and US-facing sportsbooks structure their parlay insurance differently due to regulatory environments. If you’re betting from outside the UK, verify that your jurisdiction qualifies for advertised promotions before building accumulators specifically to take advantage of insurance.

Understanding insurance mechanics at this granular level prevents disappointments where you assume you’re covered only to discover your bet didn’t qualify due to a technicality. The bookmaker’s promotional terms are legally binding contract language, not loose guidelines. They’re written to protect the bookmaker’s interests while appearing generous to casual readers. Your job as an informed bettor is reading these terms completely before relying on insurance as part of your betting strategy.

How Acca Insurance Works: The Fine Print Matters

The devil in acca insurance lives in details that bookmakers bury in terms and conditions rather than highlighting in marketing materials. These restrictions, qualifications, and conditions determine whether insurance genuinely adds value or whether it’s smoke and mirrors that changes your behavior without meaningfully reducing risk.

Minimum odds requirements per selection create the first significant restriction. Most insurance offers require each leg to meet a threshold, typically 1.30 or 1.40 in decimal odds. This prevents you from building accumulators entirely from heavy favorites, which the bookmaker knows have high probability of winning. You can’t stack five selections at 1.15 each and expect insurance coverage you need to include odds that involve genuine uncertainty.

This requirement fundamentally changes accumulator construction if you’re targeting insurance qualification. Instead of naturally selecting the outcomes you genuinely fancy, you’re selecting outcomes that meet arbitrary odds thresholds set by the bookmaker. Sometimes these align you might independently assess that several selections around 1.80 represent value. Other times they don’t align, and you’re forcing higher-odds selections into your acca specifically to qualify for insurance rather than because they represent good bets.

Maximum refund caps limit how much you can recover regardless of your actual stake. If a bookmaker caps insurance refunds at twenty-five pounds and you stake fifty pounds on a qualifying acca, you’re only getting back half your stake if you trigger the insurance. This asymmetry means higher-stakes bettors derive less proportional value from insurance offers compared to lower-stakes bettors. Someone staking ten pounds gets full protection, while someone staking one hundred pounds gets partial protection that barely moves the needle on their overall risk profile.

Qualifying sports and markets vary dramatically between bookmakers. Some limit insurance to football accumulators only. Others include tennis, basketball, and major sports but exclude niche markets. Certain bookmakers restrict insurance to specific bet types like match results, excluding both teams to score, handicaps, or player-specific markets. If you prefer building accumulators from corner markets or card markets, you might find that no insurance offers cover your preferred betting style.

The “one leg loses” requirement seems straightforward until you encounter edge cases. What happens if one leg loses and another voids? Most bookmakers treat voids as non-events that remove the leg from your acca, so if you have a six-fold where one loses, one voids, and four win, you end up with a four-fold that lost one leg but the void might disqualify you from insurance if the promotion required six valid legs minimum. The interaction between voids and insurance qualification varies by bookmaker, creating situations where the same objective outcome qualifies at one bookie but not another.

Time-limited offers add another complexity layer. Some bookmakers run acca insurance promotions only during specific periods maybe football season weekends, major tournaments, or promotional campaigns tied to specific events. If you’re building your accumulator strategy around insurance availability, you need to track which bookmakers currently offer it and adjust your betting behavior when terms change. Relying on insurance that was available last month but isn’t available this month leads to unpleasant surprises.

Exclusions and prohibited practices hide in terms and conditions that few bettors read completely. Most insurance offers exclude related contingency betting you can’t build an acca where one selection’s outcome makes another selection’s outcome more or less likely. They exclude same-game multiples or bet builders from most insurance promotions. They prohibit obvious arbitrage or hedging strategies, though enforcing this prohibition is difficult in practice. They reserve the right to void refunds if they suspect abuse or advantage play, a catch-all that gives bookmakers discretion to deny payouts in situations they didn’t specifically enumerate.

The free bet terms attached to refunds carry their own restrictions that reduce the refund’s actual value. Free bets typically expire within seven to fourteen days, forcing you to use them quickly rather than waiting for opportunities where you identify genuine value. They often can’t be split into smaller bets if you get a twenty-pound free bet back, you need to use it on a single twenty-pound wager rather than splitting it into four five-pound bets with better risk distribution. Some free bets restrict which markets you can use them on, preventing you from placing them on extremely short-odds favorites or extremely long-odds long-shots.

Understanding all these fine-print restrictions requires actually reading the full terms and conditions document, not just the promotional headline. Bookmakers design marketing materials to emphasize benefits while downplaying restrictions. The bold text says “Money Back if One Leg Loses!” while the small print says “on qualifying 5+ leg football accumulators with minimum 1.40 odds per leg, maximum £25 refund, refunded as free bet expiring in 7 days, excludes bet builders and same-game multiples, available pre-match only.” Both statements are technically true, but they create very different impressions of what the offer actually provides.

Types of Acca Insurance Offers

Bookmakers structure their insurance promotions in several distinct ways, each with different strategic implications for bettors. Understanding these variations helps you choose which bookmaker to use for specific accumulator types and how to structure your bets to maximize insurance value.

Standard money-back insurance represents the basic model where you get your stake refunded as a free bet if exactly one leg loses. This is the most common offer across UK bookmakers, though the specific terms vary. Bet365, William Hill, Ladbrokes, and most major bookies offer some version of this promotion, typically requiring five or six selections minimum with odds around 1.30 to 1.40 per leg. The refund comes as a free bet equal to your stake up to a promotional maximum, usually twenty to fifty pounds.

Acca Edge or reduced-odds insurance works differently by offering you a choice before placing your bet. You can take standard odds with no insurance, or accept slightly reduced odds in exchange for guaranteed stake refund if one leg loses. For example, a four-fold that would normally pay at 8.00 might offer an “Edge” option at 7.20 with insurance included. You’re essentially buying insurance by accepting lower potential returns, which makes sense in some situations but not others depending on your risk preferences and the specific odds reduction involved.

Multiple-leg insurance extends protection beyond the single-leg-loses scenario. Some bookmakers offer tiered refunds if one leg loses you get full stake back, if two legs lose you get 50% stake back, if three legs lose you get 25% back. This structure creates partial protection across a wider range of near-miss outcomes, though the refund percentages mean you’re still taking substantial losses on two-leg or three-leg failures. These offers typically require longer accumulators (seven or eight selections minimum) and come with stricter odds requirements.

Early payout insurance combines insurance with conditional early settlement. If your team goes two goals ahead in football, the bookmaker settles that leg as a winner immediately even if the match later ends in a draw or defeat. This effectively removes one potential failure point from your accumulator before the match concludes. These promotions usually require substantial minimum odds per leg and exclude many markets, but they genuinely alter win probability when they trigger by converting uncertain outcomes into confirmed winners early.

Acca boost with insurance combines odds enhancement with stake refund protection. A bookmaker might offer to boost your five-fold accumulator odds by 10% while also providing insurance if one leg loses. This double promotion sounds extremely generous, but typically comes with the strictest terms high minimum odds per leg, limited qualifying sports, capped maximum stakes and refunds, and restricted customer eligibility. New customers often get access to these combined promotions that existing customers don’t see.

Loyalty program acca insurance provides ongoing insurance as a benefit of VIP or loyalty status rather than as a one-off promotion. High-volume bettors might earn permanent insurance on all qualifying accumulators as part of their customer tier benefits. These offers typically have the most favorable terms lower minimum odds requirements, higher refund caps, broader market coverage because they’re rewards for customers the bookmaker has already determined are profitable relationships.

Sport-specific insurance targets particular events or leagues. During major tournaments like the World Cup or Champions League, bookmakers run special insurance promotions with enhanced terms maybe requiring only four selections instead of five, or offering higher refund caps than normal. These tournament-specific offers create opportunities to build accumulators with better insurance value than you’d get during regular season betting, though the bookmaker knows increased betting volume during major events more than compensates for the improved terms.

Cashback versus free bet insurance represents another distinction worth understanding. Most insurance comes as free bets with all the restrictions mentioned earlier. Rare cashback insurance offers refund actual withdrawable cash instead, making them substantially more valuable. If you find a bookmaker offering cashback insurance rather than free bet insurance, the terms are almost certainly much stricter elsewhere to compensate probably very high minimum odds, very limited maximum refund, or extreme restrictions on qualifying markets.

The strategic implication of these varied structures is that different bookmakers suit different accumulator types. If you prefer conservative four-fold accumulators with modest odds, a standard insurance offer requiring five selections doesn’t help you. If you place occasional long-shot ten-folds, a multiple-leg insurance structure that provides partial refunds on two-leg or three-leg losses adds more value than standard one-leg insurance. Matching your natural betting style to appropriate insurance offers extracts more genuine value than trying to force your betting to fit whichever promotion has the flashiest marketing.

Top Bookmakers with Acca Insurance: Detailed Comparison

The UK betting market offers numerous acca insurance promotions, but they’re far from identical. Comparing major bookmakers across key dimensions helps you identify which offers best match your betting preferences and provide genuine value versus which are marketing gimmicks with impractical terms.

Bet365 offers one of the longest-running and most established acca insurance promotions. Their Soccer Accumulator Bonus applies to pre-match accumulators of three or more selections on specific soccer markets. While they don’t frame it explicitly as “insurance,” they offer bonus percentages on winning accumulators and have historically provided various accumulator-focused promotions. Their terms tend to be straightforward with clear qualification criteria, though the bonuses and protections vary by region and change periodically based on competitive landscape.

William Hill pioneered mainstream acca insurance in the UK market with their “Acca Insurance” promotion. They refund stakes up to twenty-five pounds as a free bet if one selection in a five-plus leg accumulator loses, requiring minimum 1.30 odds per leg. The offer covers football, tennis, and several other sports, though restrictions apply to specific markets within those sports. William Hill’s insurance has broad market coverage but relatively conservative refund cap compared to some competitors.

Paddy Power structures insurance through their “Money Back Special” promotions that change regularly. Rather than a permanent acca insurance offer, they run targeted promotions on specific events or leagues with varying terms. This means the best insurance deal might be with Paddy Power one week and a different bookmaker the next. Their promotional approach rewards bettors who actively shop for the best current terms rather than defaulting to one bookmaker consistently.

Betfred offers “Acca Insurance” on football accumulators with relatively generous terms refunds up to fifty pounds on qualifying bets with one losing leg. They require five or more selections with minimum odds of 1.20 per leg, which is lower than many competitors and allows more flexibility in accumulator construction. Betfred’s higher refund cap makes them attractive for higher-stakes bettors who stake more than twenty-five pounds per accumulator, though the free bet expiry terms and usage restrictions still apply.

Betway provides “Betway Boost” promotions that sometimes include insurance elements, though their offers vary significantly by time period and customer segment. They tend to focus insurance on major football leagues and tournaments rather than offering permanent broad-spectrum coverage. When their promotions are active, terms are competitive, but the inconsistency means you can’t rely on insurance being available when you want to place an accumulator.

Coral and Ladbrokes, both part of the same corporate group, offer similar insurance structures with slight variations. Their “Acca Insurance” promotions typically refund up to twenty-five pounds if one leg of a five-plus selection accumulator loses, with minimum odds around 1.30 per leg. Coverage includes football and racing primarily, with other sports occasionally added during promotional periods. Their terms are middle-of-the-road neither the most generous nor the most restrictive in the market.

Sky Bet differentiates through their “Request a Bet” feature combined with periodic insurance promotions. Rather than static terms, they allow customers to request specific accumulator combinations and get custom odds, sometimes with insurance attached during promotional periods. This flexibility can create opportunities for better-value insurance coverage on unusual accumulator structures that don’t fit standard promotion templates.

Spreadex and other trading-focused bookmakers offer insurance less frequently because their business model emphasizes different bet types. When they do run accumulator promotions, terms often favor their existing customer base of higher-stakes, more sophisticated bettors, with higher refund caps but stricter qualification criteria.

New entrant bookmakers trying to build market share often offer the most aggressive insurance terms temporarily higher refund caps, lower minimum odds, fewer restrictions as customer acquisition tools. These offers rarely sustain long-term as the bookmaker matures and optimizes profitability, but they create short windows where informed bettors can extract substantial value before terms tighten.

The practical comparison most bettors should make focuses on the insurance offers available for their specific betting patterns. If you primarily bet football accumulators of five selections with odds around 1.60 to 2.00 per leg, compare bookmakers based on that exact use case which offers best terms for that structure, highest refund cap, most favorable free bet conditions. If you prefer tennis accumulators or racing multiples, the bookmaker rankings change completely because different bookies lead in different sport coverage.

Rather than declaring one bookmaker definitively best, the strategic approach involves maintaining accounts with several bookmakers and choosing which to use for each specific accumulator based on current promotions and terms. The bookmaker with best insurance for football five-folds might have terrible terms for racing accumulators. The bookmaker with highest refund cap might have the shortest free bet expiry window. Optimizing requires matching specific bets to appropriate bookmakers rather than concentrating all your betting with one operator.

Expected Value Analysis: Does Insurance Actually Add Value

The crucial question acca insurance raises is whether it genuinely improves your expected value or whether it’s clever marketing that changes behavior without improving results. The mathematical answer depends on several factors that vary by individual bettor and specific promotion terms.

Expected value calculations for acca insurance require estimating several probabilities. First, what’s the probability your accumulator wins outright? Second, what’s the probability it loses by exactly one leg? Third, what’s the probability it loses by two or more legs? These probabilities depend on your selection count, individual selection odds, and correlation between selections.

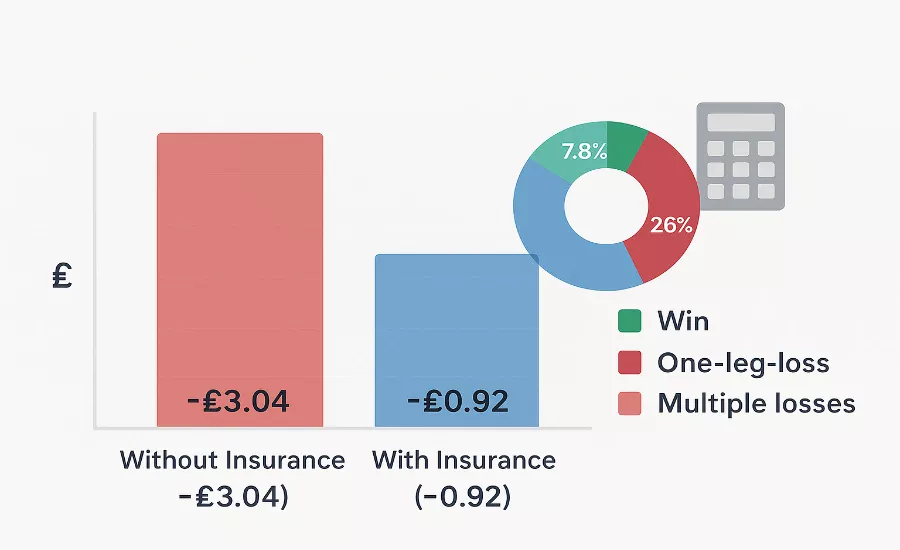

For a simplified example, imagine a five-fold accumulator where each selection has a 60% independent win probability. The probability all five win is roughly 7.8%. The probability exactly one loses is about 26%. The probability two or more lose is about 66%. Standard acca insurance refunds your stake in the 26% scenario, converting what would be total loss into partial recovery via free bet worth approximately 85% of stake value.

If you stake twenty pounds on this accumulator at combined odds of 10.00, let’s calculate expected value with and without insurance. Without insurance: 7.8% chance of winning 200 pounds, 92.2% chance of losing 20 pounds. Expected value equals approximately -3.04 pounds per bet. With insurance refunding in the one-leg-loss scenario: 7.8% chance of winning 200 pounds, 26% chance of recovering 17 pounds via free bet, 66.2% chance of losing 20 pounds completely. Expected value improves to approximately -0.92 pounds per bet.

Insurance doesn’t make the bet profitable you’re still taking negative expected value on average. But it reduces your expected loss by roughly two pounds per bet in this example. Over ten such bets, insurance saves you about twenty pounds of expected loss. That’s genuine value, even though it doesn’t transform accumulator betting into a profitable activity.

The value insurance adds varies dramatically based on your accumulator structure. Short accumulators with fewer selections and higher individual probabilities derive less benefit because the “exactly one leg loses” scenario is less probable relative to other outcomes. Long accumulators with many selections derive more benefit because near-miss scenarios become increasingly common as selection count grows.

The free bet terms affect value calculations significantly. If the refunded free bet expires quickly or comes with severe usage restrictions, its effective value drops below 85% toward 70-75%. This reduces the expected value improvement insurance provides. Conversely, if you can use free bets strategically on value selections with minimal restrictions, you might extract closer to 90% of face value, increasing insurance benefit.

Your baseline betting behavior matters for value assessment. If insurance encourages you to place more accumulator bets than you otherwise would, and those additional bets represent negative value selections you wouldn’t have made without the insurance carrot, then insurance might be decreasing your overall results despite improving individual bet EV. The behavioral economics of promotions often matter more than the pure mathematics of individual bet expected value.

Strategic use of insurance involves building accumulators specifically structured to maximize insurance value when you’re taking advantage of these promotions. This might mean adjusting your selection count toward the sweet spot where one-leg-loss probability is highest, or adjusting individual selection odds to barely meet minimum requirements while maximizing overall success probability. These optimizations extract more value from insurance offers than casually placing accumulators that happen to qualify.

For matched bettors using insurance offers for guaranteed profit extraction, the expected value equation transforms completely. Matched betting techniques involve backing accumulators with insurance then laying outcomes to guarantee profit whether the acca wins, loses by one leg, or loses by multiple legs. This requires betting exchange access, substantial capital, and careful calculation, but it converts insurance from incremental value add to profit generation engine. Most casual bettors don’t engage with this level of sophistication, but understanding that professional advantage players exploit insurance systematically reveals that these offers do contain extractable value under the right conditions.

Strategies for Maximizing Acca Insurance Value

Extracting maximum value from insurance offers requires intentional accumulator construction rather than accidentally qualifying for insurance on bets you’d place anyway. Several strategic approaches help you capture more benefit from insurance promotions while minimizing the behavioral traps they create.

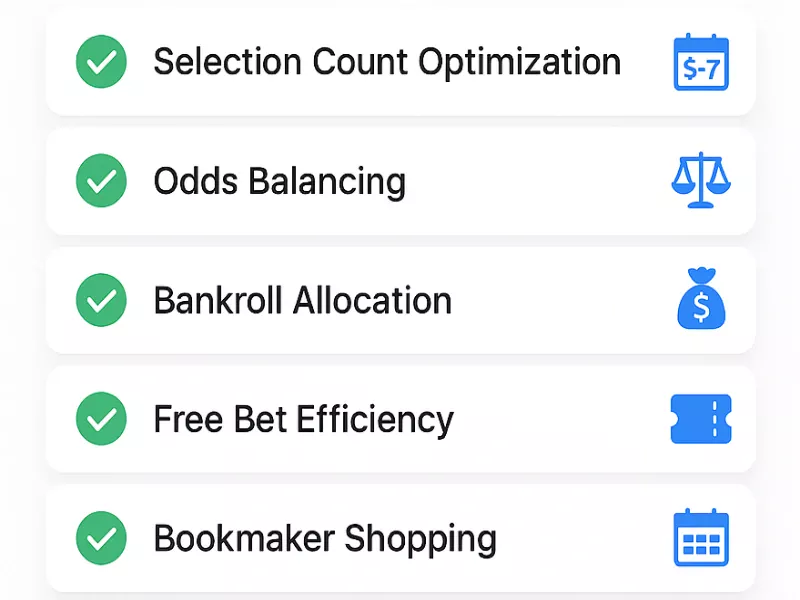

Selection count optimization targets the sweet spot where one-leg-loss probability is highest relative to complete win and multiple-leg-loss probabilities. For most accumulator structures, this sits around five to seven selections depending on individual selection odds. Fewer selections and the insurance scenario becomes relatively unlikely. Many more selections and the scenario where everything goes right becomes so improbable that insurance is irrelevant because you’re never close to winning anyway.

Odds balancing involves structuring your accumulator so individual selection odds meet insurance minimums while maximizing the overall probability that exactly one selection fails. One approach mixes four relatively safe selections around 1.40 to 1.60 odds with one riskier selection at 2.20 to 2.50 odds. If the four safe bets come through and the risky one fails, you trigger insurance. If everything hits, you get the full payout. This structure gives you two ways to avoid complete loss.

Bankroll allocation for insured accumulators justifies slightly larger stakes than uninsured accumulators because the effective risk is reduced. If insurance reduces expected loss by 30-40%, you might increase your stake by 15-20% to capture more value from favorable promotions while still maintaining conservative overall bankroll management. This doesn’t mean reckless stake increases it means modest adjustments that reflect the improved risk profile insurance creates.

Using free bet refunds efficiently maximizes the value you extract from insurance when it triggers. Don’t waste free bets on random selections placed quickly before expiry. Use them on value bets you’ve identified independently outcomes where you believe true probability exceeds the implied probability from bookmaker odds. A free bet placed on a value selection at 2.50 odds extracts more than a free bet placed on an arbitrary selection just to use it before expiration.

Bookmaker shopping means maintaining accounts with multiple bookmakers and choosing which to use for each specific accumulator based on current insurance terms. If Bookmaker A has insurance on five-plus football accumulators and Bookmaker B has insurance on four-plus tennis accumulators, you place your football accumulators at Bookmaker A and your tennis accumulators at Bookmaker B. This simple segmentation captures more insurance value than concentrating all betting with one bookmaker.

Timing your accumulators to coincide with enhanced promotional periods extracts better terms. During major tournaments, bookmakers often improve insurance conditions higher refund caps, lower minimum odds, additional sports coverage. If you’re flexible about when you place accumulators, concentrating them during these promotional windows provides better insurance value per bet.

Avoiding negative behavioral changes that insurance encourages preserves your overall betting discipline. Insurance should improve bets you’d place anyway, not cause you to place worse bets just because they’re insured. If you find yourself adding unnecessary legs to reach the five-selection minimum when you only genuinely fancy three outcomes, insurance is harming rather than helping your betting process. The goal is using insurance strategically on quality accumulators, not letting insurance availability dictate your betting behavior.

After learning how accumulator insurance works and how this feature can help reduce the risk of losing large multi-bets, readers can always return to the acca-bet to continue exploring the site’s other betting guides.

If you would like to understand why many accumulator bets still fail despite having attractive odds and apparently logical selections, it is very useful to also read the article why your acca bets keep losing.

Expertly verified: Oliver Bennett